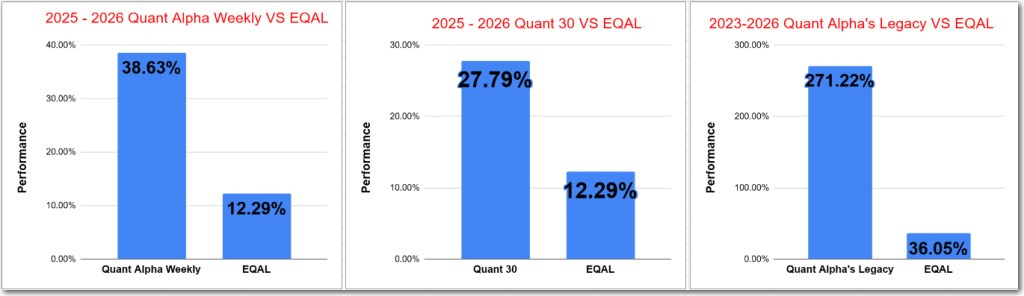

- Quant 30 – Up over 27% since June

- Quant Weekly – Up over 38% since June

- Legacy – Up over 260% since April 2023

- Education – Is AI a Bubble? – memo from Howard Marks, Dec. 9 2025

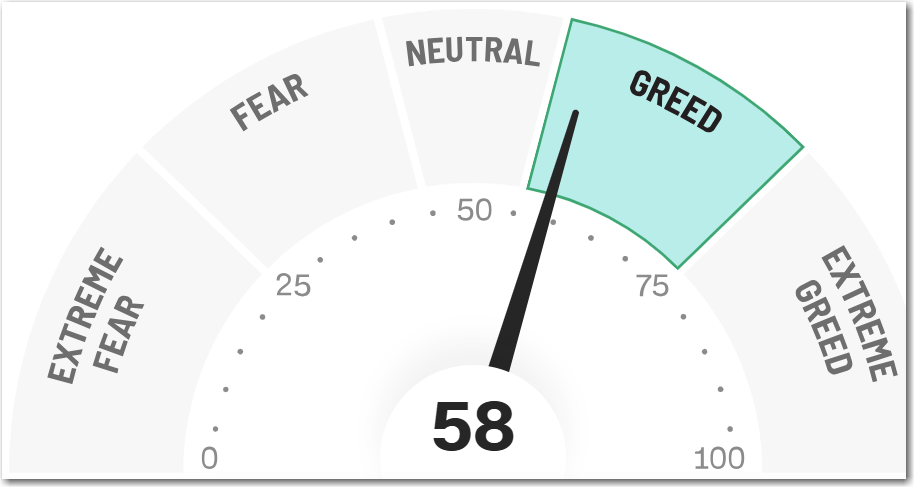

USA stock market summary for last week

Index Performance: Jan. 26 – Jan. 30, 2026

Weekly total moves (approx):

- S&P 500: +0.3% for the week to ~6,939 points.

- Nasdaq Composite: down ~0.2%.

- Dow Jones Industrial Average: down ~0.4%.

- Russell 2000: down ~2.1%.

Takeaway (Week at a Glance)

- Large-cap indexes held up better overall (S&P 500 slightly positive), but small caps weakened most sharply.

- Tech stocks lost ground, contributing to Nasdaq’s weekly decline.

- Defensive and stable sectors outperformed amid macro uncertainty, while materials and commodity-linked sectors fell sharply.

The Quant Alpha Weekly and Quant 30 portfolios closed at all-time monthly highs.

Note: This site now offers both a free and a paid subscription. Paid subscribers receive weekly Portfolio updates as soon as they’re released. Free subscribers still get full content, but Portfolio updates will be posted with at least a two-week delay. Want timely access to the new Adds/Removes? Click here.

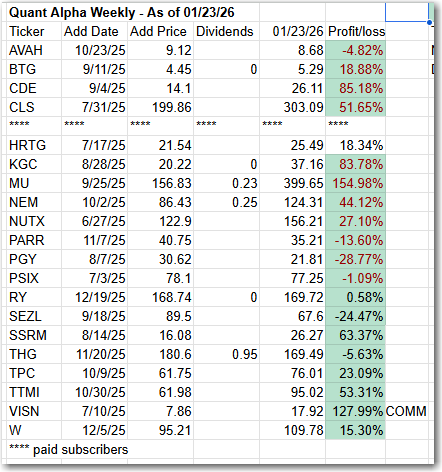

Model Portfolio Quant Alpha Weekly

The newly Added stock, if any, is being released to the Paid Subscribers today. Shown below are the updates from two weeks ago. This Portfolio continues to beat its benchmark by a wide margin, 36% to 12%.

No Adds to the Portfolio this week

Add (01/16/26) : None

Outperformers: CDE (Coeur Mining) up over 40%, MU (Micron Technology) up over 160%, VISN (Vistance Networks) up over +120%

Click here for the Quant Alpha Weekly details

Quant Weekly Performance – Weekly Summary

- Mining & tech sectors were the biggest drag on the portfolio this week.

- Energy and healthcare provided relative support, with PARR and NUTX showing upside movement.

- Most financials and industrial names were flat to slightly down in the latest session, suggesting broader market caution.

Model Portfolio Quant 30

This week’s new update, if any, is being released to the paid subscribers. Shown below is the update made two weeks ago. This Portfolio continues to beat its benchmark by a wide margin, 27% to 12%.

Three new Adds and three Removals for this update.

Add (01/16/26) : CIEN (Ciena Corp), VISN (Vistance Networks), LASR (nLIGHT)

Remove (01/16/26) : UBER, STX (Seagate Technology), BAC (Bank of America)

Outperformers: MU (Micron Technology) up over 240%, GFI (Gold Fields) up over 100% and KGC (Kinross Gold) is up over 90%.

Click here for the Quant 30 details

Model Portfolio Quant Alpha’s – Legacy

The portfolio now has around 19 stocks in it. It is up over +260% since it began in 2023. Celestica achieves a 11 bagger performance.

Remove (01/16/26): None

Outperformers: AGX (Argan) up over 400%, WGS (GeneDx Holdings) up over 200%, STRL (Sterling Infrastructure) up over 500%, POWL (Powell Industries) up over 700% and CLS (Celestica) is up over 1100%

Click here for the Quant Alpha’s – Legacy details

Performance to 01-30-2026

| Portfolio start date 6/27/25 | |

| Quant Alpha Weekly | 36.34% |

| EQAL (Russell 1000 Equal Weight ETF) | 12.24% |

| Portfolio start date 6/27/25 | |

| Quant 30 | 27.79% |

| EQAL (Russell 1000 Equal Weight ETF) | 12.24% |

| Portfolio start date 4/14/23 | |

| Quant Alpha’s – Legacy | 271.22% |

| EQAL (Russell 1000 Equal Weight ETF) | 36.00% |

Click here for the Live Quant scorecard

The Quant Alpha Weekly Portfolio remains ahead of its benchmark. Up over 36% since it began on June 27, 2025.

The Quant 30 Portfolio remains ahead of its benchmark. With new earnings reports coming out, the pace of turnover is increasing. It is up 27% since it began on June 27, 2025.

The Quant Alpha’s – Legacy Portfolio maintained its over 260% return since April 2023, in a classic Position Trading Portfolio implementation.

Is AI a Bubble? – summary of Howard Marks memo – 12/9/25

1. What a Bubble Really Is

Marks explains that a market bubble isn’t simply rising prices — it’s when investor psychology drives asset prices well above underlying intrinsic value, fueled by excessive optimism, FOMO (“fear of missing out”), and a belief that this time it’s different. Historical bubbles have followed a familiar pattern:

- A new idea or technology captures imagination

- Early investors profit

- Others rush in without rational valuation

- Prices detach from fundamentals

- The result is painful losses for many — though some winners may still emerge.

2. Is AI a Bubble?

Marks breaks the question into two parts:

- Company behavior: Some AI firms are investing aggressively without clear paths to profit.

- Investor behavior: Enthusiasm for AI has been massive, and much of recent stock-market gains have come from AI-linked stocks.

He does not definitively say AI is a bubble, but notes that today’s situation shares many characteristics of past bubbles. Memories of past crashes don’t prevent new ones, because excitement and visions of revolutionary change overwhelm prudence.

3. Good vs. Bad Bubbles

The memo introduces the idea that some bubbles — particularly those tied to transformative technologies — can have positive effects even if investors lose money. Two types are described:

- Mean-reversion bubbles: Pure financial fads that don’t change the world (e.g., the pre-2008 mortgage craze).

- Inflection bubbles: Driven by real technological change — like railroads or the internet — which can accelerate innovation and long-term progress despite short-term losses.

Marks argues that enthusiastic investment in new technologies can speed innovation by funneling capital into exploratory projects even if many fail.

4. Parallels with History

The memo draws on historical examples (internet, railroads, subprime-mortgage products) to highlight how newness and lack of historical experience make markets prone to over-optimism, driving prices far beyond what predictable earnings justify.

Marks also points out that valuations for current AI leaders are not obviously more extreme than during past bubbles (e.g., internet-era valuations), which complicates declaring today’s conditions a classic bubble.

5. Risks and Uncertainty

Marks emphasizes key uncertainties:

- Who will ultimately win in AI markets?

- How profitable will these technologies be, and when?

- How much capital will be wasted on ventures that don’t succeed?

Because the technology’s impact and timeline are unpredictable, many companies may be overvalued relative to their fundamentals, and some investors will suffer significant losses.

6. Practical Conclusion for Investors

Marks doesn’t say to fully avoid AI investments, nor does he insist it’s definitely a bubble. Instead, he suggests:

- A balanced approach: Neither all-in optimism nor complete avoidance.

- Prudence and selectivity: Recognize the potential for both transformational gains and wealth destruction.

He warns that bubbles can accelerate technological progress, but they also carry the risk of serious financial loss for those who join late or without proper risk assessment.

Bottom Line

- AI has characteristics of past bubbles — strong enthusiasm, rapid capital flows, and uncertain fundamentals — but whether today is objectively a bubble is impossible to say until later.

- The memo argues for cautious participation: understand risks, avoid blind enthusiasm, but don’t necessarily miss out on transformative advances.

Website Investment Educational Blog Posts –

All content on this site is for informational purposes only and does not constitute financial advice. Consult relevant financial professionals in your country of residence to get personalized advice before you make any trading or investing decisions. This post was written with the assistance of artificial intelligence. The original ideas and final review are human-generated. Disclaimer

Copyright 2023-2026 SwingTrader.Trading. All Rights Reserved.

You must be logged in to post a comment.