- Selection for this week

- Some Pros about the stock

- Some Cons about the stock

- Criteria for choosing

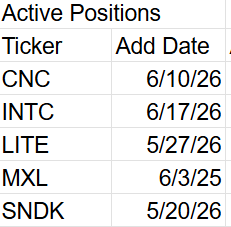

- The previous selections

Add: VICR (Vicor Corporation) – Electronic Components

What does the company do?

Vicor Corporation designs and manufactures modular power components and power systems that convert and manage electrical power. Its products serve industries including aerospace, defense, telecommunications, industrial automation, transportation, and electric vehicles. Founded in 1981, Vicor is headquartered in Andover, Massachusetts and sells its products worldwide.

Why Some Investors Are Bullish

AI power demand is driving record revenue and strong momentum.

- Q1 2026 revenue reached a record $113 million, up 20.2% year over year, with an order backlog of approximately $300.6 million.

- The company raised Q2 guidance from approximately $126 million to $142 million, signaling exceptionally strong demand visibility.

The IP licensing business could become a highly profitable growth engine.

- Licensing revenue appears to carry exceptionally high incremental margins, enhancing profitability as the business scales.

- Each new licensee can add meaningful revenue with relatively little incremental cost, creating an attractive economics profile.

The balance sheet is a genuine fortress with virtually no leverage.

- Vicor holds approximately $404 million in cash, minimal long-term debt, and a current ratio near 9.

- The strong balance sheet allows the company to fund fab expansion and R&D internally without meaningful financing risk.

Strong margins provide significant earnings leverage.

- Q1 2026 gross margin was approximately 55%, among the stronger profitability profiles in power electronics.

- As higher-margin licensing revenue becomes a larger contributor, there is potential for additional margin expansion.

Capacity expansion and IP enforcement are creating a multi-year competitive moat.

- Vicor is expanding manufacturing capacity through investments in its first CHiP fab and planning a second facility.

- Active protection and monetization of its intellectual property could create additional long-term revenue opportunities.

What Bears Are Worried About

Valuation is extremely demanding.

- The stock trades at premium valuation levels, including a P/E above 100 and Price-to-Sales around 27.

- These valuation multiples require continued strong execution and leave little room for disappointment.

Founder control limits shareholder influence.

- CEO Patrizio Vinciarelli controls approximately 79.1% of total voting power through the dual-class share structure.

- Minority shareholders have limited influence over board composition, strategic decisions, and capital allocation.

Customer concentration and manufacturing concentration create execution risk.

- A meaningful portion of revenue has historically been derived from a limited number of large customers.

- Until the second fab is operational and the customer base broadens, order delays or production disruptions could materially impact results.

Bottom Line

Vicor combines strong AI-driven demand, exceptional financial strength, and a potentially lucrative licensing business with premium valuation and execution risks. The investment case largely depends on the company’s ability to continue executing at a level that justifies the market’s high expectations.

Top Quant Stock of the Week Criteria

I am using a Quantitative research platform that provides a daily list of top-ranked stocks to buy or sell, based on a Comprehensive Quant Score. This Quant system uses computer algorithms to come up with its rankings. This score incorporates multiple factors, including valuation, growth, profitability, momentum, and EPS revisions.

I will be giving heavy weight to strong momentum and strong EPS revisions to make the weekly selection. Then, I will use my tested proprietary criteria to sort and then break any tie.

One stock will be selected each week. That would make 52 selections a year if I don’t miss any weeks because of internet problems.

The hold times for the stocks added will be 1 week to years. Although a 1 week hold would be rare, it could happen if the stocks Quant metrics took a big nose dive right after being selected. If an added stock maintains its good metrics, it will be kept in the portfolio until it doesn’t. No time limit. The Quant system will tell me when it is time to let it go. So the hold time is short, medium and long depending on the Quant system metrics.

All countries are included. ADR’s are ok but Pink Sheet stocks will not be allowed.

Certain Industries are excluded. My testing shows they do not perform well using Quantitative rankings. Two of the main ones are BioTechnology and Pharmacueticals.

The Remove Criteria: Once the stock no longer qualifies to be retained in the Portfolio, it will be removed. This could be because the companies metrics have deteriorated since selection, it is involved in a buyout or financial reporting problems.

Once a stock has been added to the Active list, it will not be added to. No doubling down.

The stocks considered are larger small cap, mid cap, large cap and Mega cap. They will be fairly easy to trade with opening or closing market orders as one of the ways to enter and exit positions.

It should be expected that about 50 stocks will be Active in the Portfolio in any given week, once it gets to the two year mark.

All stocks are added as equal weight. No rebalancing is to occur.

To be considered for addition, the stock has to be in the top group of Quant rankings for just several weeks. This is to allow newly upgraded stocks to qualify quickly. Hopefully, this will catch a couple of strong momentum stocks early in their move.

Once a stock is removed for cause, it can be added back in once it meets the add criteria. No waiting period is required.

There will be no limits on percentages of stocks in the Portfolio by Sector or Industry.

Previous Selections:

All content on this site is for informational purposes only and does not constitute financial advice. Consult relevant financial professionals in your country of residence to get personalized advice before you make any trading or investing decisions. This post was written with the assistance of artificial intelligence. The original ideas and final review are human-generated. Disclaimer

Copyright 2023-2026 SwingTrader.Trading. All Rights Reserved.